Pakistan is currently facing another economic crisis, and the government is negotiating a new bailout package with the International Monetary Fund (IMF). However, such packages often come at a significant cost to the population, as they result in increased financial burden through various measures.

The government justifies these measures as necessary for stabilizing the economy and promises to bring about reform and recovery.

While some may attribute Pakistan’s economic struggles to the ongoing political crisis, the root of the problem runs much deeper. To gain a better understanding of why Pakistan finds itself in such a dire situation while its regional neighbors thrive, it is crucial to examine the country’s relationship with international trade.

The underlying causes of the crisis

On February 3, 2023, the State Bank of Pakistan’s foreign exchange reserves dropped to $2.9 billion from a peak of $20.1 billion in August 2021. This sharp decline in reserves raises concerns among investors and currency speculators, who fear the risk of an economic default. Consequently, this has led to the depreciation of the currency exchange rate.

Pakistan’s economic crisis is mainly due to the government’s inability to meet its external debt obligations, which is linked to the country’s trade imbalance. Pakistan’s current account, an essential component of the balance of payments that reflects the country’s net trade in goods and services, has consistently shown large deficits over the years. The FY22 current account deficit stood at $17.4 billion, with imports exceeding exports by about $45 billion. However, the $31.3 billion in remittances cushioned the impact.

The trade deficit, which is due to Pakistan’s exports being worth only 45% of its imports, is a significant cause of the economic crisis. Several factors contribute to this imbalance, including inefficiencies in various markets such as labor and capital. Pakistani producers cannot compete productively with foreign producers, particularly those in the neighboring Asian region, due to these inefficiencies.

Absence of industrial development

The World Bank’s recent report titled “From Swimming in Sand to High and Sustainable Growth: A Roadmap to Reduce Distortions in the Allocation of Resources and Talent in the Pakistani Economy” highlights the low productivity levels in non-agricultural sectors of Pakistan.

This not only contributes to the ongoing economic crisis but also discourages investments in the country that could enhance productivity. This lack of productivity negatively affects Pakistan’s ability to compete in the world market, especially in terms of generating exports, which has remained stagnant in comparison to its peers.

Industrialization is a critical component of a country’s economic growth, and the level of industrialization can be measured by manufacturing value added (MVA) per capita. This measure reflects the contribution of the manufacturing sector to a country’s GDP. The UNIDO often uses MVA per capita to determine the level of industrialization in a country. Additionally, indicators such as MVA per capita and merchandise exports per capita are useful in evaluating a country’s capacity to produce and export manufactured goods.

Productive producers, resulting from efficient markets and higher levels of industrialization, are more likely to participate in international trading activities.

This is particularly true in the case of countries in the Asian region, where manufactured goods make up a significant portion of merchandise exports. Therefore, to determine industrial competitiveness, it is essential to compare the level of industrialization between Pakistan and its major Asian counterparts, such as India, Bangladesh, Vietnam, and Cambodia.

Vietnam is a well-known success story when it comes to industrial competitiveness, but Cambodia has also seen significant export growth over the past decade. The analysis presented in this report relies on data from the World Development Indicators (WDI) and the World Integrated Trade Solution (WITS) to examine the manufacturing value added (MVA) per capita, population, merchandise exports and imports, as well as tariffs imposed on imports and exports for Pakistan, India, Bangladesh, Vietnam, and Cambodia.

Figure 1 shows the MVA per capita for the selected countries. In 2000, Pakistan had higher values than both Bangladesh and Cambodia but lower values than India and Vietnam. However, in 2021, Pakistan had the lowest value amongst the five countries, indicating a decline in industrialization relative to Bangladesh and Cambodia.

Figure 2 illustrates the percentage growth in manufacturing value added (MVA) per capita for the selected countries between 2000 and 2021.

During this period, Pakistan has only doubled its MVA per capita, while India has almost tripled it. On the other hand, Bangladesh, Cambodia, and Vietnam have more than quadrupled their MVA per capita. The stagnant level of industrialisation in Pakistan has significant implications for the economy, especially as the country continues to experience a recurrent balance of payments crisis.

The Trade Angle

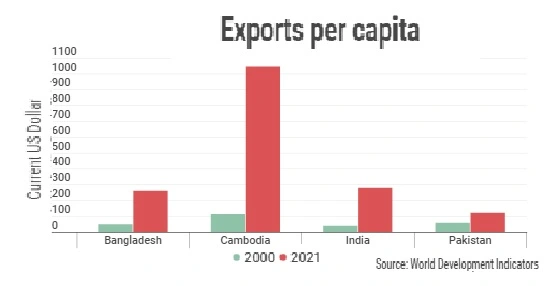

Figure 3 illustrates the exports per capita of the selected countries. In 2021, Bangladesh, Cambodia, and India reported an exports per capita value of over $260, while Pakistan’s value was $122.

In the year 2000, Pakistan’s per capita exports were higher than that of India and Bangladesh. However, Vietnam’s figures have not been included to maintain scale as it had already surpassed $3000 in 2021.

The fourth figure depicts the percentage growth in exports per capita for the selected countries between 2000 and 2021. During this time frame, Vietnam has seen an astounding increase of 1,800 percent in its exports per capita. In contrast, Pakistan’s growth rate is meager, with only a 100 percent rise in the same period.

Percentage Growth

Figure 5 displays the percentage growth in exports per capita between 2000 and 2021 for various regions. Pakistan’s performance was lower than the regional average for sub-Saharan Africa, Latin America, and the Caribbean. These regions have encountered their own obstacles that have restricted their capacity to enhance their level of industrialisation, putting them behind the economies of Asia.

In contrast to its Asian peers, Pakistan reports a lower level of imports per capita. This implies that Pakistani firms have low trade participation and productive capacity. Moreover, this indicates the limited ability of Pakistani businesses to compete in the global and regional markets.

Import tariff rates

Underperformance compared to its peers is due to its businesses’ inability to leverage trade potential with partner countries. Inefficiencies in various markets have led to high costs of doing business, along with trade barriers. Additionally, higher tariffs imposed on goods and imports by Pakistan have limited the participation of Pakistani firms in international trade activities.

Figure 7 presents the weighted average tariff rates on imported goods for the selected countries. While all the countries have decreased their average tariff rates over the past two decades, Vietnam, Cambodia, and India have made larger reductions than Pakistan and Bangladesh. Vietnam has almost completely eliminated tariff rates on imports, allowing it to integrate better into global value chains.

However, Pak has some of the highest tariff rates, with some products having rates exceeding 1,000 percent. Additionally, Pakistan has the most tariff lines above 15 percent compared to the other selected countries. In contrast, Bangladesh follows a more uniform tariff policy across products, with a maximum rate of 25 percent in 2021. As a result, Bangladesh does not report any tariff lines with rates three times higher than the simple average tariff rate. The high tariff rates imposed by Pakistan limit the participation of Pakistani businesses in international trade activities, especially when coupled with the already high cost of doing business and market inefficiencies.

{kind=link}

Pakistan currently totally crisis